Conventional Loan Requirements can feel easier with the right help. Learn what you need, avoid surprises and start your pre approval today in Tulsa now.

Many Tulsa home buyers start with the same questions: Do I need 20% down? What credit score do I need? Will I have to pay PMI? Is a conventional loan better than FHA, VA, or USDA financing?

Conventional Loan Requirements can feel confusing because they depend on more than one number. Credit, income, debt-to-income ratio, down payment, property type, appraisal, conforming loan limits, and underwriting all work together.

A conventional loan can help qualified buyers purchase or refinance a home, but approval, rates, payments, closing costs, PMI, and final terms are not guaranteed. Final loan terms depend on credit, income, debt, assets, property value, loan program rules, lender requirements, market conditions, appraisal, title review, and underwriting.

What Are Conventional Loan Requirements?

Conventional Loan Requirements usually include credit review, income verification, debt-to-income ratio, down payment, assets, appraisal, property eligibility, and conforming loan limit review. The right loan option depends on your credit, income, property, budget, down payment, and long-term homeownership goals.

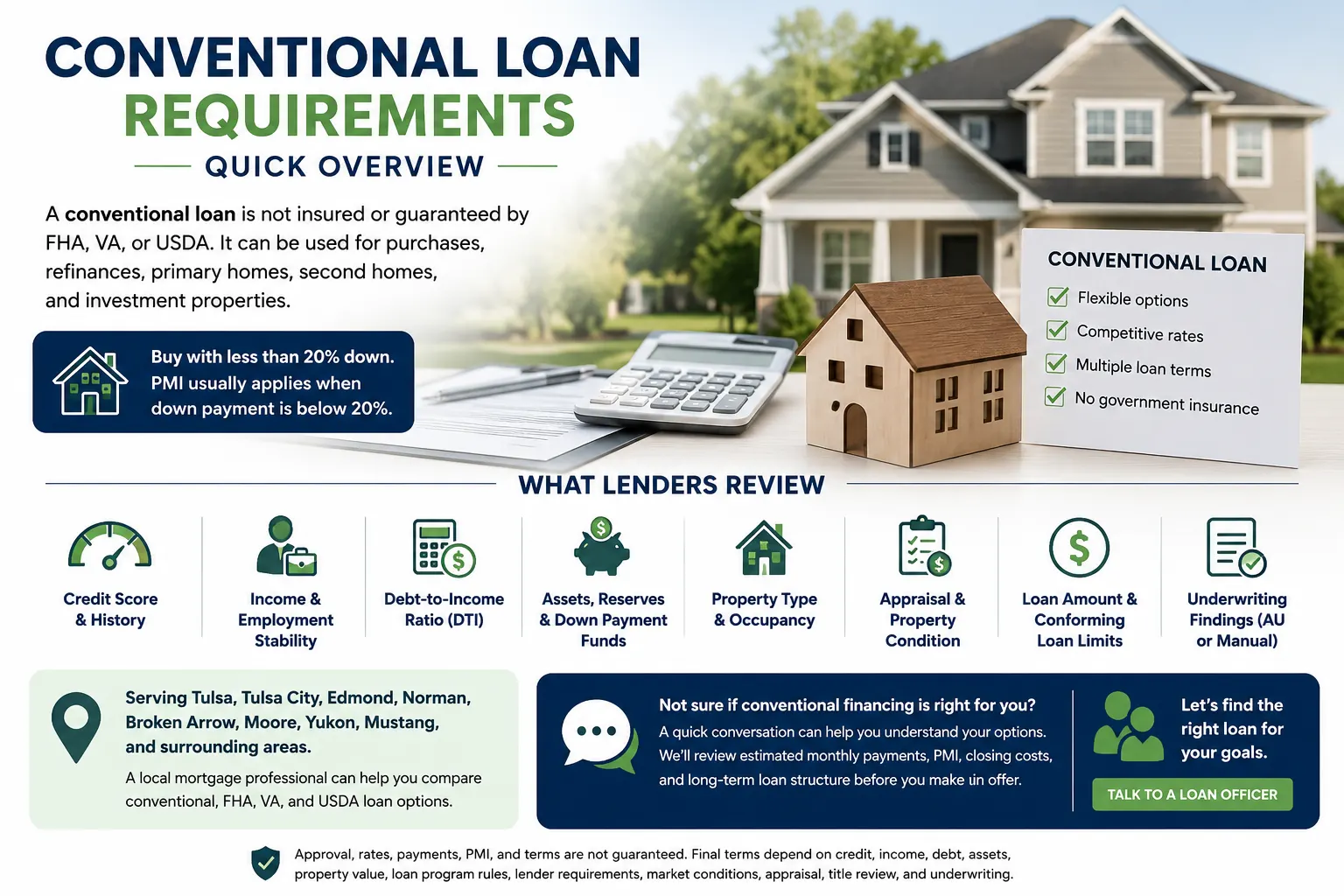

Conventional Loan Requirements: Quick Overview

A conventional loan is a mortgage that is not insured or guaranteed by FHA, VA, or USDA. Many conventional loans follow Fannie Mae or Freddie Mac guidelines, but lender requirements can still vary.

Conventional loans may be used for primary residences, second homes, investment properties, purchases, and refinances, depending on program rules. Some qualified borrowers may be able to buy with less than 20% down, but private mortgage insurance, also called PMI, usually applies when the down payment is below 20%.

Lenders usually review:

Credit score and credit history

Income and employment stability

Debt-to-income ratio

Assets, reserves, and down payment funds

Property type and occupancy

Appraisal and property condition

Loan amount and conforming loan limits

Automated or manual underwriting findings

For buyers in Tulsa, Tulsa City, Edmond, Norman, Broken Arrow, Moore, Yukon, Mustang, and surrounding Tulsa markets, a local mortgage professional can help compare conventional financing with FHA, VA, and USDA loan options.

If you are unsure whether conventional financing fits your credit, income, down payment, and home buying timeline, a short conversation can help you understand your next step. A loan officer can also help you compare estimated monthly payment, PMI, closing costs, and long-term loan structure before you make an offer.

Talk With a Conventional Loan Expert

What Is a Conventional Loan?

A conventional loan is a mortgage that is not directly backed by a government agency. FHA, VA, and USDA loans are government-backed programs, while conventional loans are usually backed by private lenders and may follow Fannie Mae or Freddie Mac rules.

Many conventional loans are conforming loans, meaning they meet investor and loan limit requirements. Non-conforming conventional loans, such as jumbo loans, may have different credit, down payment, reserve, debt-to-income, and documentation requirements.

Conventional loans can be used by first-time buyers, repeat buyers, refinancing homeowners, and some buyers purchasing second homes or investment properties. Buyers can review the official Fannie Mae Selling Guide for detailed conventional mortgage guidelines.

Madrid Mortgage Team also provides local guidance on conventional loan options for Tulsa home buyers who want help comparing programs before applying.

Key Conventional Loan Requirements to Understand

Conventional mortgage requirements are not based on one factor alone. A strong credit score may help, but income, DTI, assets, appraisal, occupancy, and underwriting still matter.

Conventional Loan Factor | What It Means | Why It Matters |

|---|---|---|

Credit score | Lenders review your score and full credit history. | Credit can affect eligibility, pricing, PMI, and documentation. |

Down payment | Your upfront investment affects loan-to-value ratio. | Lower down payments may require PMI. |

PMI | Private mortgage insurance may apply below 20% down. | PMI can affect monthly payment and total loan cost. |

Income verification | Lenders review income stability and documentation. | Income helps confirm ability to repay. |

Debt-to-income ratio | DTI compares monthly debts with qualifying income. | High DTI can affect approval options. |

Assets and reserves | Funds for down payment, closing costs, and possible reserves are reviewed. | Some files may require stronger cash reserves. |

Appraisal | The property value and condition are reviewed. | The home must support the loan request. |

Conforming loan limits | Loan amount may need to fit FHFA limits. | Loans above limits may require jumbo financing. |

Best next step | Get reviewed before house hunting. | Pre approval can help clarify your price range and loan options. |

Requirements can change and may vary by lender, loan program, borrower profile, property type, occupancy, and underwriting findings. A mortgage pre approval review can help you understand what may apply to your situation.

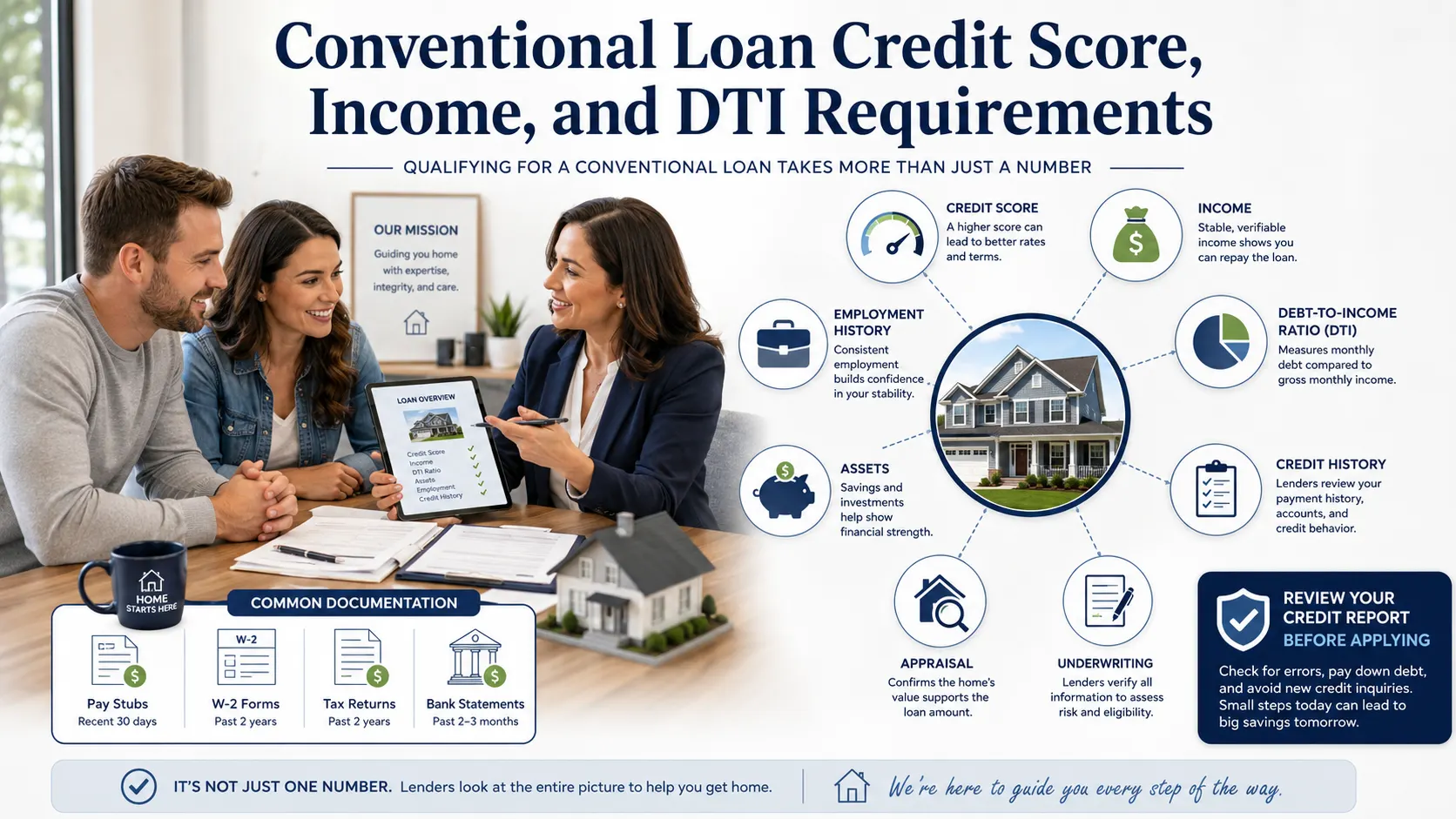

Conventional Loan Credit Score, Income, and DTI Requirements

Conventional loans usually require a full credit review. Lenders look at both the credit score and the broader credit history, including payment patterns, account history, debts, and recent credit activity.

Fannie Mae provides guidance on credit score requirements, but lender overlays can still vary. A higher score may affect pricing, PMI cost, documentation, and available loan options.

Income is also reviewed carefully. Common documents may include pay stubs, W-2 forms, tax returns, bank statements, asset statements, or business income records. Self-employed borrowers may need additional documentation.

Debt-to-income ratio, often called DTI, compares monthly debts with qualifying income. Fannie Mae’s debt-to-income ratio guidance explains how debt ratios are evaluated within conventional underwriting.

No buyer should assume approval based only on income or credit score. Lenders also review assets, employment history, down payment source, property details, appraisal, and automated underwriting findings.

Before applying, buyers can review their credit reports through AnnualCreditReport.com to check for errors or outdated information.

Conventional Loan Down Payment and PMI Requirements

One of the biggest myths about conventional loans is that every buyer needs 20% down. Some conventional loan options may allow qualified borrowers to buy with less than 20% down, depending on the full loan profile.

When the down payment is below 20%, private mortgage insurance usually applies. PMI protects the lender, not the borrower, and the cost can vary based on credit score, down payment, loan amount, property type, occupancy, and other factors.

Fannie Mae explains private mortgage insurance information for home buyers, and Freddie Mac provides a helpful overview of down payment and PMI information.

PMI may be removable later if requirements are met, but removal should not be treated as automatic in every situation. Buyers should compare total loan cost, not only the down payment.

Gift funds or assistance may be allowed depending on program rules, documentation, and borrower profile. A mortgage professional can review the Loan Estimate, cash to close, and monthly payment before you decide which loan structure fits best.

Conforming Loan Limits, Appraisal, and Property Requirements

Many conventional loans are conforming loans, meaning they must meet FHFA loan limits and Fannie Mae or Freddie Mac requirements. Conforming loan limits can change annually and may vary by county.

The Federal Housing Finance Agency publishes conforming loan limit information so buyers and lenders can verify current limits. Loans above conforming limits may be considered jumbo or non-conforming loans, which may have different requirements.

Conventional loans usually require an appraisal unless an appraisal waiver or alternative valuation option is allowed. The appraisal helps review property value, marketability, and condition.

Property requirements can differ for primary residences, second homes, investment properties, condos, manufactured homes, and multi-unit properties. Fannie Mae provides property eligibility guidance for conventional loans.

Buyers should not assume a home will qualify before lender and appraisal review. This is especially helpful in competitive Tulsa-area markets where older homes, repairs, or property type can affect the loan process.

If you are comparing purchase prices, down payment options, PMI, and property types, a local review can help you avoid surprises before making an offer. A conventional loan expert can help you understand whether the home and loan structure appear to fit current guidelines.

Talk With a Conventional Loan Expert

Conventional Loan Closing Costs and Loan Estimates

Conventional loan closing costs may include lender fees, title fees, appraisal fees, recording fees, credit report fees, prepaid property taxes, homeowners insurance, and escrow setup. Cash to close can vary based on purchase price, down payment, lender credits, seller credits, prepaid items, and loan structure.

The Loan Estimate helps buyers compare estimated loan terms, closing costs, cash to close, and projected payment. The CFPB provides a useful Loan Estimate explainer for understanding this document.

The Closing Disclosure provides final loan details before closing. Buyers can review the CFPB’s Closing Disclosure explainer to understand what to look for before signing.

Buyers should compare total loan cost, not just the interest rate. A lower rate does not always mean the best overall fit if fees, PMI, points, cash to close, or long-term plans tell a different story.

Is a Conventional Loan Good for First-Time Home Buyers?

Conventional loans are not only for repeat buyers. Some first-time buyers may qualify for low down payment conventional options, depending on credit, income, assets, property, and underwriting.

First-time buyers should compare credit requirements, down payment, PMI, closing costs, monthly payment, appraisal requirements, and long-term plans. They should not assume FHA is always better or that conventional is always better.

The best loan is the one that fits the buyer’s full financial profile and home purchase strategy. Tulsa buyers who are preparing for their first purchase can also review first-time home buyer guidance before applying.

Conventional Loan vs FHA, VA, and USDA Loans

A conventional loan may make sense when a buyer has qualifying credit, stable income, down payment funds, and property goals that fit conventional guidelines. It may also be worth reviewing for buyers considering a primary residence, second home, investment property, or refinance.

Still, another loan type may be worth comparing. FHA may help some buyers who need more flexible credit or down payment options. VA may help eligible veterans, active-duty service members, and eligible surviving spouses. USDA may help eligible rural or suburban buyers who meet location and income rules.

Madrid Mortgage Team can help buyers compare mortgage loan options, including FHA loan options, VA loan options, and USDA loan benefits.

Buyers should compare PMI, mortgage insurance, funding fees, guarantee fees, closing costs, monthly payment, appraisal standards, and long-term costs. No loan type is automatically better for every borrower.

Common Mistakes to Avoid With Conventional Loan Requirements

Conventional loans can be a strong fit for many Tulsa buyers, but mistakes during the planning stage can create delays or disappointment.

Assuming 20% down is always required

Assuming PMI is permanent

Comparing only the interest rate

Ignoring closing costs

Ignoring debt-to-income ratio

Assuming credit score alone guarantees approval

Not reviewing conforming loan limits

Not preparing income and asset documents

Forgetting about possible reserve requirements

Ignoring appraisal and property requirements

Not comparing Loan Estimates

Choosing a loan before getting pre approved

Home buyers should choose a loan based on total fit, not just one feature like down payment, PMI, or interest rate. The better question is how the loan fits your credit, cash to close, monthly budget, property, and long-term goals.

```

Real-Life Conventional Loan Requirement Scenarios in Oklahoma

```

1. Tulsa First-Time Buyer Comparing Conventional and FHA

A Tulsa first-time buyer may have limited down payment savings but decent credit and steady income. In this situation, the buyer may compare conventional and FHA options to understand down payment, PMI, mortgage insurance, closing costs, and monthly payment.

This example is hypothetical and does not guarantee approval, savings, or a specific payment. The right choice would depend on credit, income, debt, assets, property, pricing, and underwriting.

2. Tulsa City Move-Up Buyer Trying to Reduce PMI

A Tulsa City move-up buyer may have equity from a current home sale and want to reduce or avoid PMI with a larger down payment. The buyer may still need to review DTI, reserves, loan amount, appraisal, and closing costs.

This example is not a promise that PMI can be avoided. The final loan structure would depend on the purchase price, down payment, loan program, lender requirements, and underwriting findings.

3. Broken Arrow Buyer Comparing Primary Residence and Investment Property

A Broken Arrow buyer may want to compare conventional loan requirements for a primary residence versus an investment property. Investment property financing may require different down payment, reserve, credit, and pricing considerations.

This example is educational only. Loan terms and approval depend on the full borrower profile, property type, appraisal, market conditions, and lender requirements.

```

How to Prepare for Conventional Loan Pre Approval

```

Preparing for conventional loan pre approval should include reviewing your credit, down payment funds, income documents, employment history, DTI, assets, reserves, property goals, PMI, conforming loan limits, closing costs, monthly payment, and long-term cost.

Before applying, gather recent pay stubs, W-2 forms, tax returns if needed, bank statements, identification, asset documentation, and information about your target purchase price. Self-employed borrowers may need additional business and tax documentation.

A mortgage professional can compare conventional loan options, FHA loan options, VA loan options, USDA loans, down payment assistance, refinance options, cash out refinance, and other home loan programs.

If you are close to buying, a pre approval review can help you understand your buying power before you spend weekends touring homes. It can also help you compare loan structure, estimated cash to close, and next steps with more confidence.

Talk With a Conventional Loan Expert

```

Conventional Loan Requirements FAQs for Tulsa and Oklahoma Home Buyers

```

What are conventional loan requirements?

Conventional loan requirements usually include credit review, income verification, DTI review, down payment funds, asset documentation, property eligibility, appraisal review, conforming loan limit review, and underwriting approval. Requirements can vary by lender, program, property, and borrower profile.

What credit score do you need for a conventional loan?

Conventional loans usually require a credit score review, but the exact requirement depends on the loan program, lender overlays, occupancy, down payment, and underwriting findings. Buyers should not assume approval based only on credit score.

Do conventional loans require 20% down?

No, 20% down is not always required. Some qualified borrowers may use a lower down payment conventional option, but PMI usually applies when the down payment is below 20%.

When is PMI required on a conventional loan?

PMI is usually required when a conventional borrower puts less than 20% down. PMI cost can vary based on credit score, loan amount, down payment, occupancy, property type, and loan structure.

What DTI is needed for a conventional loan?

DTI requirements can vary by loan program, borrower profile, credit, assets, property, and underwriting findings. A lender reviews monthly debts compared with qualifying income to help determine whether the payment appears affordable.

Do conventional loans have income limits?

Many standard conventional loans do not have the same type of income limits as some assistance or affordable lending programs. However, income must be documented and acceptable for underwriting.

Is a conventional loan better than FHA?

A conventional loan is not always better than FHA, and FHA is not always better than conventional. The better choice depends on credit, down payment, PMI or mortgage insurance, closing costs, property type, approval strength, and long-term goals.

Should I get pre approved before house hunting?

Yes, getting pre approved before house hunting can help you understand your estimated price range, documentation needs, loan options, and possible cash to close. Final approval still depends on underwriting, appraisal, title review, and program requirements.

Last Updated: 3rd June 2026

Reviewed By: Alfredo Madrid, NMLS #266006