Explore the USDA Loan Eligibility Map to see if a property may qualify. Review income rules, eligible areas, and next steps. Start your loan review today.

Many Tulsa-area buyers hear about USDA loans because they may allow qualified borrowers to buy a home with no required down payment. The next question is usually simple: does the home’s location qualify?

The USDA Loan Eligibility Map can help buyers check whether a property near Broken Arrow, Bixby, Owasso, Claremore, Coweta, Glenpool, Sapulpa, or other surrounding areas appears to be in a USDA-eligible location. However, the map is only one part of the USDA loan process.

A property may appear eligible on the map, but that does not guarantee loan approval, borrower eligibility, income eligibility, property approval, rates, payments, closing costs, or final loan terms. Final loan results depend on property location, household income, credit, debt, assets, household size, program rules, lender requirements, appraisal, title review, and underwriting.

This guide explains how the USDA map works, how Tulsa buyers can check an address, what requirements apply beyond the map, how income limits work, and when to compare USDA financing with FHA, VA, and conventional loan options.

What Is the USDA Loan Eligibility Map?

The USDA Loan Eligibility Map is an online USDA tool used to check whether a property appears to be located in a USDA-eligible area. It can help buyers review property location, but map results are not a final approval decision and must be confirmed through the official loan process.

How Does the USDA Loan Eligibility Map Work?

The USDA loan eligibility map allows buyers, lenders, and real estate professionals to search a property address or browse a general area. The map helps show whether a location appears to fall inside or outside a USDA-eligible zone.

USDA eligibility is based on rural area rules, property location, and program guidelines. Some suburban areas around Tulsa may qualify, while some areas that look rural may not qualify. That is why the exact property address matters.

Buyers near Tulsa, Tulsa City, Broken Arrow, Bixby, Jenks, Owasso, Sand Springs, Claremore, Glenpool, Sapulpa, Coweta, Wagoner, Collinsville, Skiatook, and nearby communities should not rely on city names alone. USDA eligibility can vary by boundary, neighborhood, and exact location.

The map can also change when USDA updates eligible and ineligible areas. Current USDA loan guidelines, property boundaries, and eligible areas should always be verified before applying or making an offer.

If you are unsure whether a property may fit USDA financing, a quick review can help you understand your next step. A USDA loan professional can review the map result, income limits, buyer profile, and loan options before you move forward.

Why Does USDA Property Eligibility Matter?

USDA loans are designed for eligible rural and some suburban properties. The property must generally be used as the borrower’s primary residence, and location is one of the first eligibility checks.

Property eligibility is separate from borrower eligibility. A home may appear eligible on the map, but the buyer must still meet income, credit, debt, documentation, appraisal, and underwriting requirements.

Buyers can use the official USDA Income and Property Eligibility Site to begin reviewing property and income eligibility. The site is helpful, but it should not replace a full lender review.

For Tulsa-area buyers, checking the address early can prevent wasted time. If USDA financing is part of the plan, it is better to review the property before making an offer rather than after the contract is already signed.

How Can Tulsa Buyers Check a Property Address on the USDA Map?

Tulsa buyers can use the USDA map as an early research tool before house hunting or making an offer. The process is simple, but the result should still be reviewed with a mortgage professional.

Go to the official USDA eligibility tool.

Select the Single Family Housing property eligibility option.

Enter the property address as accurately as possible.

Review whether the location appears eligible or ineligible.

Check nearby areas if you are flexible on location.

Save or note the result for your lender review.

Do not treat the map result as final approval.

The official USDA property eligibility map can help buyers search by address. If the result appears promising, the next step is to review the buyer’s income, debt, credit, and full USDA loan profile.

One useful tip is to check the exact address, not just the city. A home in one part of a community may have a different result from a home nearby, depending on the current USDA boundary.

What USDA Loan Requirements Apply Beyond the Map?

The USDA Loan Eligibility Map only helps with location review. A complete USDA loan review includes both the property and the borrower.

USDA guidelines can change, and requirements may vary by loan program, lender, property, household size, borrower profile, and underwriting findings. Buyers should confirm current requirements before applying.

USDA Eligibility Factor | What It Means | Why It Matters |

|---|---|---|

Property location | The home must appear to be in a USDA-eligible area. | Location is one of the first USDA checks. |

Household income | USDA reviews income based on household size and area rules. | A buyer can find an eligible home but still exceed income limits. |

Credit review | Lenders review credit score, history, and payment patterns. | Credit can affect documentation and underwriting. |

Debt-to-income ratio | DTI compares monthly debts with qualifying income. | Debt level can affect approval strength. |

Primary residence | The home is generally expected to be owner-occupied. | USDA loans are not designed for investment properties. |

Appraisal | The property value and condition are reviewed. | The home must meet program and lender requirements. |

Approved lender review | A participating lender reviews the full loan file. | The map alone does not approve the borrower. |

Closing costs | Costs can include lender, title, appraisal, prepaid, and escrow items. | No down payment does not mean no cash may be needed. |

Best next step | Review the property and buyer profile before making an offer. | Early review can reduce surprises. |

USDA Rural Development publishes program guidance and resources through official channels, including USDA Rural Development handbooks. A local mortgage professional can help translate those rules into practical next steps for your situation.

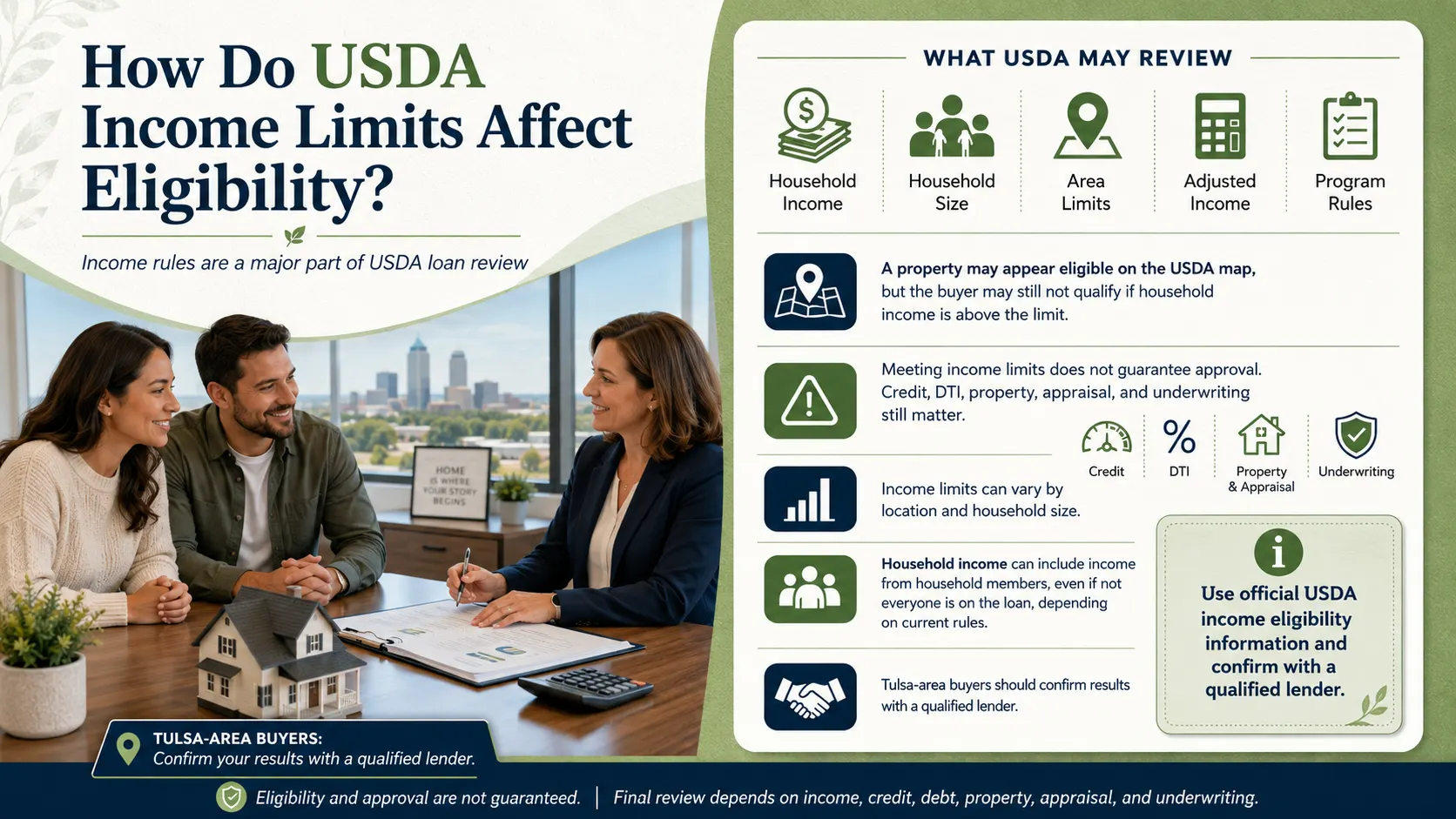

How Do USDA Income Limits Affect Eligibility?

USDA income eligibility is a major part of the approval review. USDA may evaluate household income, household size, area limits, adjusted income, and program rules.

This means a buyer may find a property that appears eligible on the USDA map but still not qualify if the household income is above the applicable limit. A buyer may also meet income limits but still need to satisfy credit, DTI, property, appraisal, and underwriting requirements.

Income limits can vary by location and household size. Buyers should use official USDA resources, such as USDA income eligibility information, and then confirm the results with a qualified lender.

For Tulsa-area buyers, household income can be more detailed than expected. Income from household members may need to be reviewed even if not everyone will be on the loan, depending on current USDA rules and documentation requirements.

Can USDA Loans Help Buyers Purchase With No Down Payment?

USDA loans may allow qualified borrowers to purchase with no required down payment, subject to property eligibility, income eligibility, lender review, and underwriting. This can be helpful for eligible buyers who want to conserve cash while buying a primary residence.

However, no required down payment does not mean no cost. Closing costs, prepaid taxes, homeowners insurance, escrow setup, appraisal fees, title fees, and other expenses may still apply.

The official USDA Single Family Housing Guaranteed Loan Program page explains the purpose of the guaranteed loan program. Buyers should also compare program costs, possible guarantee fees, monthly payment, and cash-to-close expectations.

A Loan Estimate can help buyers compare loan terms, projected payment, closing costs, and estimated cash to close. The CFPB provides a helpful Loan Estimate explainer for understanding this document.

If you are comparing USDA with FHA, VA, or conventional financing, a loan review can help you understand more than just the down payment. You can compare closing costs, loan structure, monthly payment, and long-term fit before choosing a path.

What Areas Near Tulsa May Be Worth Checking on the USDA Eligibility Map?

Some areas around Tulsa may be worth checking because USDA eligibility is location-specific. Buyers should not assume a city, suburb, or rural-looking area qualifies without checking the official USDA map.

Communities that buyers may research include Broken Arrow, Bixby, Jenks, Owasso, Sand Springs, Claremore, Glenpool, Sapulpa, Coweta, Wagoner, Collinsville, Skiatook, and other surrounding areas. Eligibility can vary by exact property address.

In some cases, one side of a road, neighborhood, or boundary may differ from another. That is why USDA address lookup is more useful than relying on a general idea of whether an area feels rural or suburban.

Can a Suburban Home Near Tulsa Qualify for USDA Financing?

Some suburban homes may appear USDA eligible, but eligibility depends on the exact property address, current USDA map boundaries, income limits, and loan requirements. A lender review is still needed before relying on USDA financing for an offer.

How Does USDA Compare With FHA, VA, and Conventional Loans?

USDA may fit buyers looking in eligible rural or suburban areas who meet income and property rules. It can be a helpful option for qualified low-to-moderate income buyers who want to review no down payment mortgage possibilities.

FHA may be worth comparing for buyers who need flexible credit or down payment options. VA may be worth comparing for eligible veterans, active-duty service members, and eligible surviving spouses. Conventional loans may be worth comparing for buyers with qualifying credit, income, and down payment goals.

Madrid Mortgage Team can help buyers review USDA loan options alongside broader mortgage loan options, including FHA loan options, VA loan options, and conventional loan options.

USDA resources also connect buyers to the broader USDA Single Family Housing Programs category. Buyers should compare down payment, mortgage insurance, guarantee fees, funding fees, PMI, closing costs, property rules, and long-term costs before deciding.

What Mistakes Should Buyers Avoid When Using the USDA Loan Eligibility Map?

The USDA map is useful, but it can create confusion if buyers treat it as a full approval tool. It should be used as an early research step, not as the final decision.

Assuming the map guarantees loan approval

Checking only the city instead of the exact property address

Ignoring USDA income limits

Assuming every rural-looking property qualifies

Assuming every suburban property is ineligible

Forgetting that the property must meet USDA requirements

Ignoring appraisal and property condition

Not checking household income correctly

Waiting too long to get pre approved

Comparing only down payment instead of total loan cost

Not reviewing a Loan Estimate

Not asking how USDA compares with FHA, VA, and conventional options

Use the USDA eligibility map as a starting point, not as the final loan decision. The strongest approach is to review the map, income limits, buyer profile, property condition, and full Loan Estimate together.

What Real-Life USDA Eligibility Map Scenarios Can Tulsa Buyers Learn From?

Could a Broken Arrow Buyer Use the USDA Map Before Making an Offer?

A Broken Arrow buyer may find a property on the edge of a growing suburban area and want to know whether USDA financing may work. In this hypothetical situation, the buyer should check the exact address on the USDA map before assuming the property fits the program.

This example does not guarantee property eligibility or loan approval. The buyer would still need a full review of household income, credit, debt, appraisal, property condition, and underwriting.

Could an Owasso Buyer Qualify If the Property Appears Eligible?

An Owasso buyer may find a home that appears to be in an eligible location. That is a helpful first step, but property eligibility is only one part of the USDA loan review.

The buyer’s household income, credit history, DTI, employment, documentation, and loan file would still need to be evaluated. Final eligibility is subject to USDA review, lender requirements, appraisal, title review, and underwriting.

Could a Claremore Buyer Compare USDA With FHA or Conventional?

A Claremore buyer may compare USDA with FHA or conventional financing based on location, income limits, down payment, closing costs, monthly payment, and long-term goals. USDA may be worth reviewing, but it is not automatically better for every buyer.

This example is educational only. The right loan option depends on the buyer’s full financial profile, the property, program rules, and current market conditions.

How Should Buyers Prepare Before Applying for a USDA Loan?

Preparing before applying can make the USDA loan process easier to understand. Buyers should review both the property and borrower side of the file before house hunting too far into the process.

Helpful preparation steps include reviewing:

The exact property address

The USDA map result

Household income and household size

Credit history and monthly debts

Employment history and income documents

Bank statements and available funds

Cash-to-close expectations

Appraisal and property condition

Loan Estimate details

Long-term affordability

Buyers can also review mortgage pre approval steps before shopping and read first-time home buyer guidance if this is their first purchase.

USDA also provides resources for USDA Active Lenders, while buyers can review credit reports through AnnualCreditReport.com before applying.

If you are looking at homes near Tulsa and want to know whether USDA financing may fit, a local review can help you connect the map result with income, credit, debt, and property requirements. Personalized guidance can help you avoid relying on the map alone.

What Questions Do Tulsa Buyers Ask About the USDA Loan Eligibility Map?

What Is the USDA Loan Eligibility Map?

The USDA Loan Eligibility Map is an official tool that helps buyers check whether a property appears to be located in a USDA-eligible area. It is useful for early research, but it does not guarantee loan approval or final property eligibility.

How Do I Check a Property on the USDA Eligibility Map?

You can enter the exact property address into the USDA property eligibility tool and review whether the location appears eligible or ineligible. You should still ask a lender to review the property, income, and borrower profile.

Does the USDA Map Guarantee Loan Approval?

No. The USDA map does not guarantee loan approval, borrower eligibility, property eligibility, income eligibility, rates, payments, or closing costs. Final review depends on the complete loan file.

Can Homes Near Tulsa Qualify for USDA Loans?

Some homes near Tulsa may appear eligible, especially in certain rural or suburban areas. Eligibility depends on the exact address, current USDA map boundaries, income limits, property requirements, and underwriting.

What If a Property Looks Eligible on the USDA Map?

If a property looks eligible, the next step is to review income eligibility, credit, DTI, employment, assets, appraisal, and documentation. A property result is only one part of the USDA loan process.

Do USDA Loans Have Income Limits?

Yes. USDA income limits can vary by location, household size, and program rules. Buyers should confirm current limits before applying because income eligibility is separate from property eligibility.

Can I Use a USDA Loan With No Down Payment?

USDA loans may allow qualified borrowers to buy with no required down payment, subject to eligibility, lender review, property approval, and underwriting. Closing costs and prepaid items may still apply.

Should I Get Pre Approved Before Using the USDA Map to Shop for Homes?

Yes. The USDA map can help you search locations, but pre approval helps review your income, credit, debts, documents, and estimated price range. Final approval still depends on the full loan process.

What Should Buyers Know Before Publishing or Relying on This USDA Map Guide?

USDA Loan Eligibility Map information is educational only and should be reviewed for accuracy by a licensed mortgage professional before publishing. USDA map results do not guarantee property eligibility, borrower eligibility, income eligibility, loan approval, rates, payments, savings, closing costs, or loan terms.

Loan approval depends on property eligibility, income eligibility, credit, income, debt, assets, household size, property value, loan program rules, lender requirements, appraisal, title review, and underwriting. Information may change, so buyers should confirm current USDA guidelines, map boundaries, income limits, property rules, closing costs, and program requirements.

The CFPB’s Closing Disclosure explainer can help buyers review final loan details before closing.

Last Updated: 3rd June 2026

Reviewed By: Alfredo Madrid , NMLS #266006