FHA Streamline Refinance helps eligible FHA borrowers compare rate options, reduce paperwork, and move faster. Check savings and apply today online now.

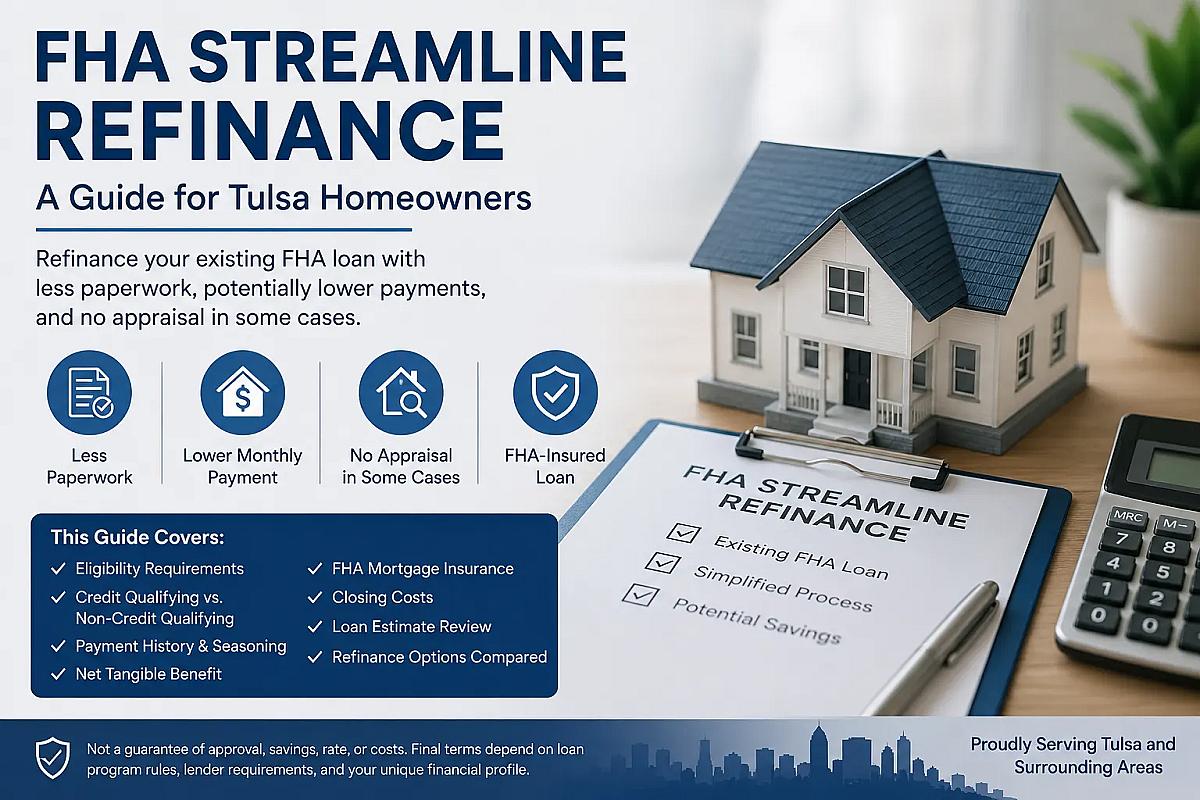

Many Tulsa-area homeowners with an existing FHA loan wonder whether they can refinance with less paperwork, lower their monthly mortgage payment, or avoid a traditional appraisal. That is why the FHA Streamline Refinance is often searched by homeowners who already have an FHA-insured mortgage.

An FHA streamline refinance can help eligible homeowners refinance from one FHA-insured loan into another FHA-insured loan with limited documentation and underwriting compared with some other refinance types. However, the word “streamline” does not mean automatic approval, no costs, guaranteed savings, or guaranteed payment reduction.

This guide explains FHA streamline refinance eligibility, existing FHA loan requirements, credit qualifying and non-credit qualifying options, payment history, seasoning, net tangible benefit, FHA mortgage insurance, closing costs, Loan Estimate review, appraisal considerations, and comparison with FHA cash out refinance, FHA simple refinance, and conventional refinance.

FHA streamline refinance eligibility, approval, rates, payments, savings, closing costs, appraisal requirements, mortgage insurance, and final terms are not guaranteed. Final terms depend on the existing FHA loan, payment history, seasoning, credit, income when required, loan program rules, lender requirements, market conditions, title review, and underwriting.

What Is an FHA Streamline Refinance?

An FHA Streamline Refinance is a refinance option for eligible homeowners with an existing FHA-insured mortgage. It may require less documentation and underwriting than some other refinance types, but streamline does not mean automatic approval, guaranteed savings, no appraisal in every case, or no closing costs.

How Does an FHA Streamline Refinance Work?

An FHA streamline refinance is designed for homeowners who already have an FHA-insured mortgage. The goal is to refinance the current FHA loan into a new FHA-insured loan under applicable FHA and lender rules.

The “streamline” part usually refers to reduced documentation and underwriting compared with some other refinance programs. It does not mean the loan skips all review. The lender still needs to confirm the existing FHA loan status, payment history, refinance purpose, title details, costs, and program eligibility.

Some FHA streamline refinance files may not require a traditional appraisal, depending on program rules and lender requirements. Some files may be non-credit qualifying, while others may require credit qualifying review.

For homeowners in Tulsa, Tulsa City, Broken Arrow, Bixby, Jenks, Owasso, Sand Springs, Claremore, Glenpool, Sapulpa, Coweta, Wagoner, Collinsville, Skiatook, and nearby Oklahoma markets, a local refinance review can help connect the FHA rules with the homeowner’s actual mortgage situation.

If you are unsure whether your current FHA loan may qualify, a short conversation can help you understand your options before you spend time comparing rates or offers. A mortgage professional can review your current loan, payment history, refinance goal, closing costs, and possible net tangible benefit.

Check FHA Streamline Refinance Options

Who Can Qualify for an FHA Streamline Refinance?

The homeowner generally must already have an FHA-insured mortgage. In many cases, the refinance is an FHA-to-FHA refinance, meaning the current FHA loan is replaced with a new FHA-insured loan.

Payment history matters because FHA streamline refinance is not designed to ignore serious mortgage payment concerns. Seasoning requirements may also apply, meaning the existing FHA loan usually needs to meet timing and payment-history rules before refinance eligibility can be confirmed.

The refinance must usually provide a net tangible benefit to the homeowner. This benefit may involve payment, rate structure, loan term, or another qualifying refinance result, depending on current FHA rules and the loan file.

HUD provides official FHA streamline refinance information for homeowners and mortgage professionals. A lender review is still needed because program rules, lender requirements, and underwriting findings can vary.

What FHA Streamline Refinance Requirements Should Homeowners Understand?

An FHA streamline refinance is usually simpler than some refinance options, but it still has requirements. Homeowners should understand the main review factors before assuming the refinance is automatically available.

FHA Streamline Refinance Factor | What It Means | Why It Matters |

|---|---|---|

Existing FHA loan | The homeowner generally needs a current FHA-insured mortgage. | FHA streamline refinance is built for FHA-to-FHA refinancing. |

Payment history | The lender reviews recent mortgage payment behavior. | Late payments can affect eligibility. |

Seasoning | The current FHA loan may need to meet timing rules. | A loan may be too new to refinance immediately. |

Net tangible benefit | The refinance usually must provide a recognized benefit. | The loan should have a clear refinance purpose. |

Credit qualifying review | Some files require credit and capacity review. | Documentation may be more detailed. |

Non-credit qualifying review | Some files may involve reduced credit documentation. | This can make the process simpler for eligible homeowners. |

Appraisal | A traditional appraisal may not be required in some cases. | No appraisal is not guaranteed for every file. |

Closing costs | Refinance costs may still apply. | Streamline does not mean no-cost refinance. |

Best next step | Review the current loan and new Loan Estimate. | This helps compare short-term and long-term fit. |

Requirements can change and may vary by loan program, lender, borrower profile, payment history, current FHA loan, and underwriting findings.

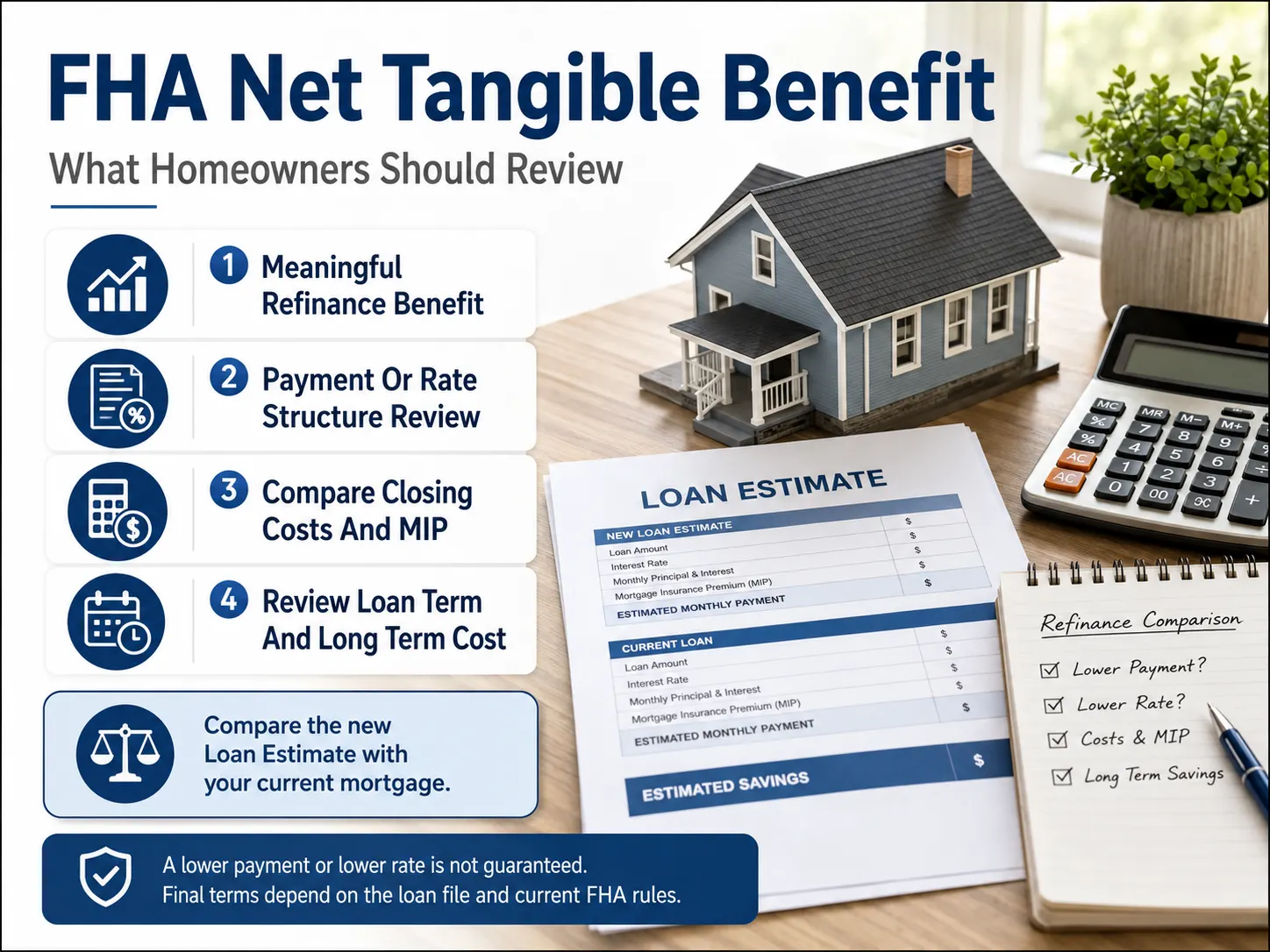

What Is the FHA Net Tangible Benefit Requirement?

An FHA streamline refinance usually needs to provide a net tangible benefit. In simple terms, the refinance should provide a meaningful benefit that meets FHA program rules.

Net tangible benefit may relate to payment reduction, rate structure, loan term, or refinance purpose depending on current rules. A lower payment is not guaranteed, and a lower interest rate does not always mean the best total outcome.

Homeowners should review closing costs, mortgage insurance, loan term, escrow changes, and long-term cost. Comparing the new Loan Estimate with the current mortgage situation is one of the best ways to understand whether the refinance makes sense.

The FHA Single Family Housing Policy Handbook is an official FHA policy source, but homeowners should work with a mortgage professional to apply current rules to their own file.

Does an FHA Streamline Refinance Require an Appraisal?

One reason homeowners search for FHA streamline refinance is because some streamline refinance options may not require a traditional appraisal. This can be helpful for homeowners who are unsure about current property value or do not want a full valuation process.

Still, no appraisal is not guaranteed in every situation. Lender requirements, title review, loan amount, refinance structure, and FHA program rules can still affect what must be reviewed.

Homeowners should not assume appraisal rules before lender confirmation. The official Federal Housing Administration resources can help homeowners understand the broader FHA program, but file-specific review is still needed.

What Costs Apply to an FHA Streamline Refinance?

Streamline does not mean no closing costs. Possible costs may include lender fees, title fees, recording fees, prepaid items, escrow setup, mortgage insurance, and other refinance-related costs.

FHA streamline refinance may involve upfront mortgage insurance premium and annual mortgage insurance premium depending on the file and current FHA rules. HUD provides official FHA mortgage insurance premium information for homeowners who want to understand MIP structure.

Some homeowners hear the phrase “no-cost refinance.” That does not always mean there are no costs. Costs may be handled through pricing, lender credits, or loan structure, so the total loan picture should be reviewed carefully.

The CFPB explains that a Loan Estimate gives borrowers key information about estimated interest rate, monthly payment, and closing costs. Homeowners should compare monthly payment, cash to close, loan term, mortgage insurance, and long-term cost before deciding.

If your goal is to reduce payment or simplify your current FHA loan, the next step is to compare the new refinance offer with your current mortgage. A local FHA refinance review can help you understand whether the numbers support your short-term and long-term goals.

Check FHA Streamline Refinance Options

What Documents May Be Needed for an FHA Streamline Refinance?

FHA streamline refinance may require less documentation than some other refinance types, but less documentation does not mean no documentation. The lender may still ask for information needed to confirm the loan file.

Possible documents may include the current mortgage statement, homeowner identification, homeowners insurance information, payoff details, title-related information, and escrow information. Income, employment, assets, or credit documentation may be needed if the file is credit qualifying or if lender requirements apply.

Credit qualifying streamline refinances may require more review than non-credit qualifying options. Homeowners should ask what documents are required before assuming the process will be simple for every file.

How Does FHA Streamline Refinance Compare With Other Refinance Options?

FHA streamline refinance may fit homeowners who already have an FHA loan and want to review an FHA-to-FHA refinance option. It may be useful when the homeowner wants to evaluate payment, loan term, mortgage insurance, closing costs, and possible net tangible benefit.

Other options may also be worth comparing. An FHA simple refinance may be considered when a different structure or appraisal review is needed. An FHA cash out refinance may be considered by homeowners who want to access equity, but it has different rules, costs, and risks.

Homeowners can compare mortgage refinance options with FHA loan options and broader home loan programs. Some homeowners may also compare conventional refinance options, VA loan options, or USDA loan options if they are eligible.

HUD also provides information related to FHA homeowner refunds and FHA-to-FHA refinances, while its refinance premium information can help homeowners review premium-related topics.

No refinance option is automatically better for every homeowner. The right decision depends on the current FHA loan, equity, payment goals, mortgage insurance, closing costs, credit profile, and long-term plans.

What Mistakes Should Homeowners Avoid With FHA Streamline Refinance?

An FHA streamline refinance can be helpful for some homeowners, but it should not be treated as an automatic savings tool. The details matter.

Assuming streamline means automatic approval

Assuming streamline means no closing costs

Assuming no appraisal applies to every file

Ignoring net tangible benefit

Comparing only the interest rate

Ignoring FHA mortgage insurance

Ignoring total loan cost

Extending the loan term without reviewing long-term impact

Not reviewing the Loan Estimate

Not asking whether the file is credit qualifying or non-credit qualifying

Assuming cash back is allowed like a cash out refinance

Not comparing FHA streamline with FHA simple refinance, FHA cash out refinance, or conventional refinance

Homeowners should use FHA streamline refinance as a way to compare options, not as an automatic savings guarantee. The better question is whether the new loan fits the homeowner’s payment, costs, mortgage insurance, loan term, and long-term goals.

The CFPB also explains that no-closing-cost refinance offers still involve costs in some form, so homeowners should review how the refinance is structured.

What Real-Life FHA Streamline Refinance Scenarios Can Tulsa Homeowners Learn From?

Could a Broken Arrow Homeowner Review FHA Streamline Refinance to Lower Payment?

A Broken Arrow homeowner with an existing FHA loan may want to review whether a new FHA refinance could reduce monthly payment. In this hypothetical example, the homeowner should compare payment, closing costs, MIP, loan term, and net tangible benefit before deciding.

This does not guarantee approval, savings, or payment reduction. The final result depends on the current FHA loan, market conditions, payment history, lender requirements, and underwriting.

Could an Owasso Homeowner Refinance Without a Traditional Appraisal?

An Owasso homeowner may be interested in FHA streamline refinance because some files may not require a traditional appraisal. That can be useful, but no appraisal is not guaranteed for every homeowner.

The lender still reviews the loan file, title details, program rules, existing FHA loan, and refinance structure. The homeowner should confirm appraisal requirements before assuming the property value review is unnecessary.

Could a Claremore Homeowner Compare FHA Streamline With Conventional Refinance?

A Claremore homeowner may compare FHA streamline refinance with conventional refinance based on credit, equity, mortgage insurance, closing costs, and long-term goals. A conventional refinance may or may not be a better fit depending on the full profile.

This example is educational only. Homeowners should compare loan options with actual Loan Estimates and lender guidance before making a final choice.

How Should Homeowners Prepare Before Applying for an FHA Streamline Refinance?

Preparation can help homeowners avoid confusion and compare refinance options more clearly. The first step is to confirm whether the current mortgage is FHA-insured and whether the payment history appears to support a refinance review.

Helpful items to review include:

Current FHA loan status

Recent mortgage payment history

Current mortgage statement

Refinance goal

Monthly payment

Interest rate and loan term

FHA mortgage insurance

Closing costs

Loan Estimate

Credit review if required

Income documents if required

Homeowners insurance and escrow details

Title questions and long-term affordability

Homeowners can also review mortgage pre approval steps if they want to understand documentation review more clearly. Reviewing credit reports through AnnualCreditReport.com can also help homeowners catch errors before applying.

If you are ready to compare your current FHA loan with a possible streamline refinance, a local review can help you understand the numbers. The goal is to compare payment, costs, MIP, loan term, and long-term fit before you move forward.

Check FHA Streamline Refinance Options

What Questions Do Tulsa Homeowners Ask About FHA Streamline Refinance?

What Is an FHA Streamline Refinance?

An FHA streamline refinance is a refinance option for eligible homeowners with an existing FHA-insured mortgage. It may require less documentation and underwriting than some other refinance types, but approval and savings are not guaranteed.

Who Qualifies for an FHA Streamline Refinance?

Homeowners generally need an existing FHA-insured mortgage and must meet FHA and lender requirements. Payment history, seasoning, net tangible benefit, and the type of streamline refinance can affect eligibility.

Does FHA Streamline Refinance Require an Appraisal?

Some FHA streamline refinance options may not require a traditional appraisal, but this is not guaranteed for every file. Lender rules, program requirements, and refinance structure still matter.

Does FHA Streamline Refinance Require Income Verification?

Some non-credit qualifying streamline files may require less income documentation, but homeowners should not assume income verification is never needed. Credit qualifying files or lender overlays may require more documentation.

Does FHA Streamline Refinance Require a Credit Check?

Some FHA streamline refinances may be non-credit qualifying, while others require credit qualifying review. The lender can explain which path applies based on the file and current requirements.

What Is Net Tangible Benefit for FHA Streamline Refinance?

Net tangible benefit means the refinance must provide a recognized benefit under FHA rules. It may relate to payment, rate structure, term, or refinance purpose, but it should be confirmed before applying.

Can I Get Cash Back With an FHA Streamline Refinance?

FHA streamline refinance is not designed like a cash out refinance. Homeowners who want to access equity should compare other refinance options and review the risks, costs, and requirements carefully.

Should I Compare FHA Streamline Refinance With Other Refinance Options?

Yes. Homeowners should compare FHA streamline refinance with FHA simple refinance, FHA cash out refinance, conventional refinance, and other eligible options based on payment, costs, mortgage insurance, loan term, and long-term goals.

What Should Homeowners Know Before Relying on This FHA Streamline Refinance Guide?

FHA Streamline Refinance information is educational only and should be reviewed for accuracy by a licensed mortgage professional before publishing or relying on it for a loan decision.

FHA streamline refinance does not guarantee approval, payment reduction, savings, lower rate, appraisal waiver, lower closing costs, lower mortgage insurance, or final loan terms. Loan approval depends on the existing FHA-insured mortgage, payment history, seasoning, credit when required, income when required, loan program rules, lender requirements, title review, and underwriting.

Information may change, so homeowners should confirm current FHA guidelines, MIP rules, net tangible benefit rules, closing costs, and program requirements. The CFPB’s Closing Disclosure explainer can help homeowners understand final loan details before closing.

Last Updated: 3rd June 2026

Reviewed By: Alfredo Madrid , NMLS #266006