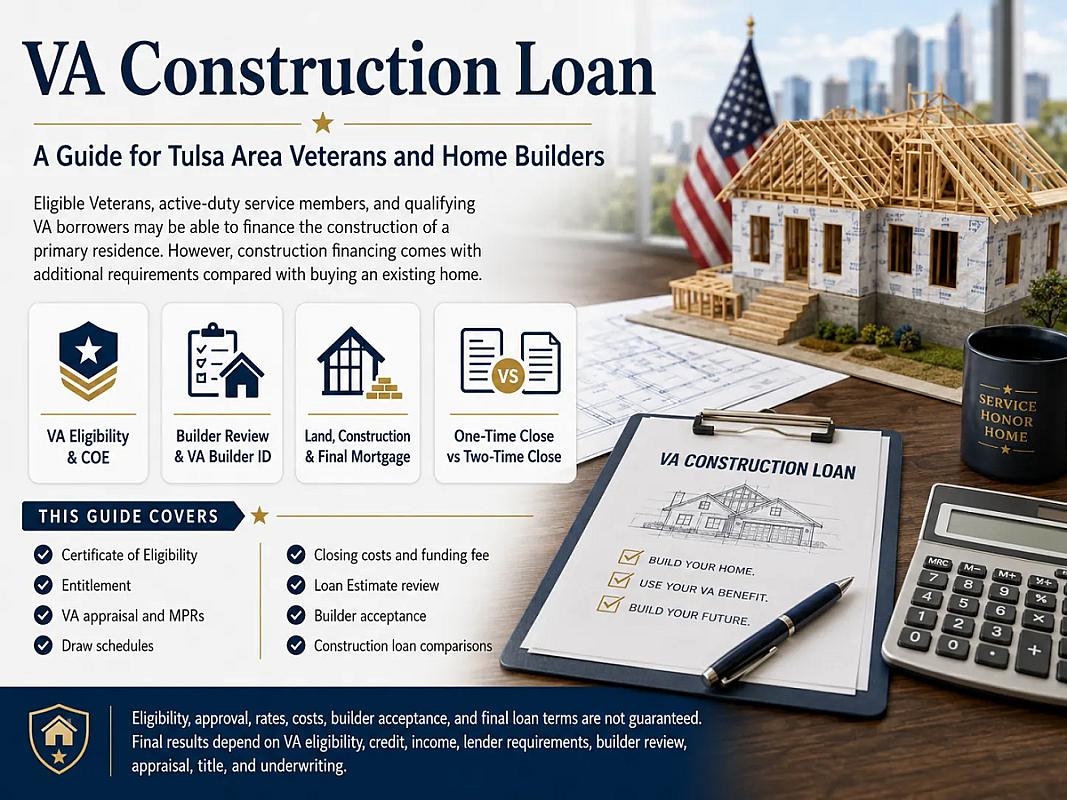

VA Construction Loan information gives you a faster path to building your home. Review key steps, avoid delays, and apply with confidence today.

Many Tulsa-area Veterans, active-duty service members, and eligible VA borrowers want to build a home instead of buying an existing property. The big question is whether VA financing can help with land, construction, the builder contract, and the final mortgage.

A VA Construction Loan may help eligible borrowers finance the construction of a primary residence using VA home loan benefits. However, construction financing usually has extra requirements compared with buying an existing home.

This guide explains VA eligibility, Certificate of Eligibility, entitlement, builder review, VA builder ID, VA appraisal, minimum property requirements, land considerations, one-time close versus two-time close financing, draw schedules, closing costs, VA funding fee, Loan Estimate review, and how VA construction financing compares with other mortgage options.

VA construction loan eligibility, approval, down payment, rates, payments, timelines, appraisal, builder acceptance, costs, and final loan terms are not guaranteed. Final results depend on VA eligibility, entitlement, credit, income, residual income, debt-to-income ratio, lender requirements, builder review, property review, appraisal, title review, market conditions, and underwriting.

What Is a VA Construction Loan?

A VA Construction Loan is a VA-backed mortgage option that may help eligible borrowers build a primary residence using VA home loan benefits. Construction financing includes extra builder, appraisal, property, title, and lender requirements, so approval is not automatic.

How Does a VA Construction Loan Work?

A VA Construction Loan is designed for eligible borrowers who want to build a primary residence instead of buying a completed home. Depending on the lender and loan structure, it may involve construction-to-permanent financing.

A one-time close construction loan may combine construction financing and permanent mortgage financing into one closing when available. A two-time close structure may involve separate construction financing first, followed by permanent mortgage financing after the home is completed.

The borrower, lender, builder, property, plans, specifications, title, land, appraisal, and construction timeline all need review. The word “VA” does not mean every lender offers this loan type, and it does not mean every builder or property will qualify.

For borrowers in Tulsa, Tulsa City, Broken Arrow, Bixby, Jenks, Owasso, Sand Springs, Claremore, Glenpool, Sapulpa, Coweta, Wagoner, Collinsville, Skiatook, and nearby Oklahoma markets, local guidance can help connect VA rules with real building decisions.

If you are thinking about building with VA benefits, review your eligibility before choosing land or signing a builder contract. A VA construction loan professional can help compare builder requirements, loan structure, construction timeline, and financing options.

Check VA Construction Loan Options

Who Can Qualify for a VA Construction Loan?

The borrower generally must be eligible for VA home loan benefits. Eligible borrowers may include qualifying Veterans, active-duty service members, eligible surviving spouses, and some National Guard or Reserve members, depending on service history and current VA rules.

A Certificate of Eligibility, often called a COE, is usually needed to show a lender that the borrower may qualify based on service history or duty status. Borrowers can review official VA home loan eligibility information before applying.

The home must generally be intended as the borrower’s primary residence. VA entitlement, credit, income, residual income, debt-to-income ratio, builder review, property review, and lender requirements may also apply.

Eligibility should be checked before choosing land, signing a builder contract, or assuming one-time close construction financing is available. Some lenders offer standard VA purchase loans but may not offer VA construction loans.

What VA Construction Loan Requirements Should Borrowers Understand?

VA construction financing involves more moving parts than a standard purchase loan. The borrower, builder, property, land, construction plans, appraisal, title, and final home completion all matter.

VA Construction Loan Factor | What It Means | Why It Matters |

|---|---|---|

VA eligibility | The borrower must generally be eligible for VA home loan benefits. | VA eligibility is the starting point for the loan review. |

Certificate of Eligibility | The COE helps show qualifying service or eligibility status. | Lenders usually need it before completing VA loan approval. |

Entitlement | Entitlement helps determine how much VA loan benefit may be available. | It can affect loan structure and lender review. |

Primary residence | The completed home is generally intended for owner occupancy. | VA loans are not designed for investment construction projects. |

Builder review | The builder may need a VA builder ID or lender-accepted review. | Not every builder can participate in every loan structure. |

Plans and specifications | The lender reviews construction plans, costs, and project details. | The property must be reviewed before the home is completed. |

VA appraisal | The appraisal may be based on plans, specs, and completed value. | Value and property requirements affect loan approval. |

Land or lot review | The lot, title, access, and ownership structure may be reviewed. | Land details can affect how the loan is structured. |

Construction draws | Funds may be released in stages as construction progresses. | Draw schedules help manage builder payments and progress. |

Best next step | Review eligibility, builder, land, and loan structure early. | Early review can reduce problems before contract signing. |

Borrowers can also review official VA home loan overview resources to understand the broader VA home loan benefit. Requirements can change and may vary by VA rules, lender, borrower profile, builder, property type, construction structure, location, and underwriting findings.

Why Does the Builder Matter for VA Construction Financing?

VA construction financing usually requires a qualified builder. Depending on current VA and lender requirements, the builder may need to be VA-registered, have a VA builder ID, or pass a lender-accepted builder review.

Borrowers should not assume every builder can participate in VA construction financing. A lender may review the construction contract, plans, budget, draw schedule, permits, licensing, insurance, builder risk coverage, and timeline.

Change orders and cost overruns should be discussed before closing. A small change in materials, finish level, timeline, or site work can affect the total project cost.

VA provides construction and valuation resources related to appraisal and valuation topics. Borrowers should still work with a VA loan professional before signing a builder contract.

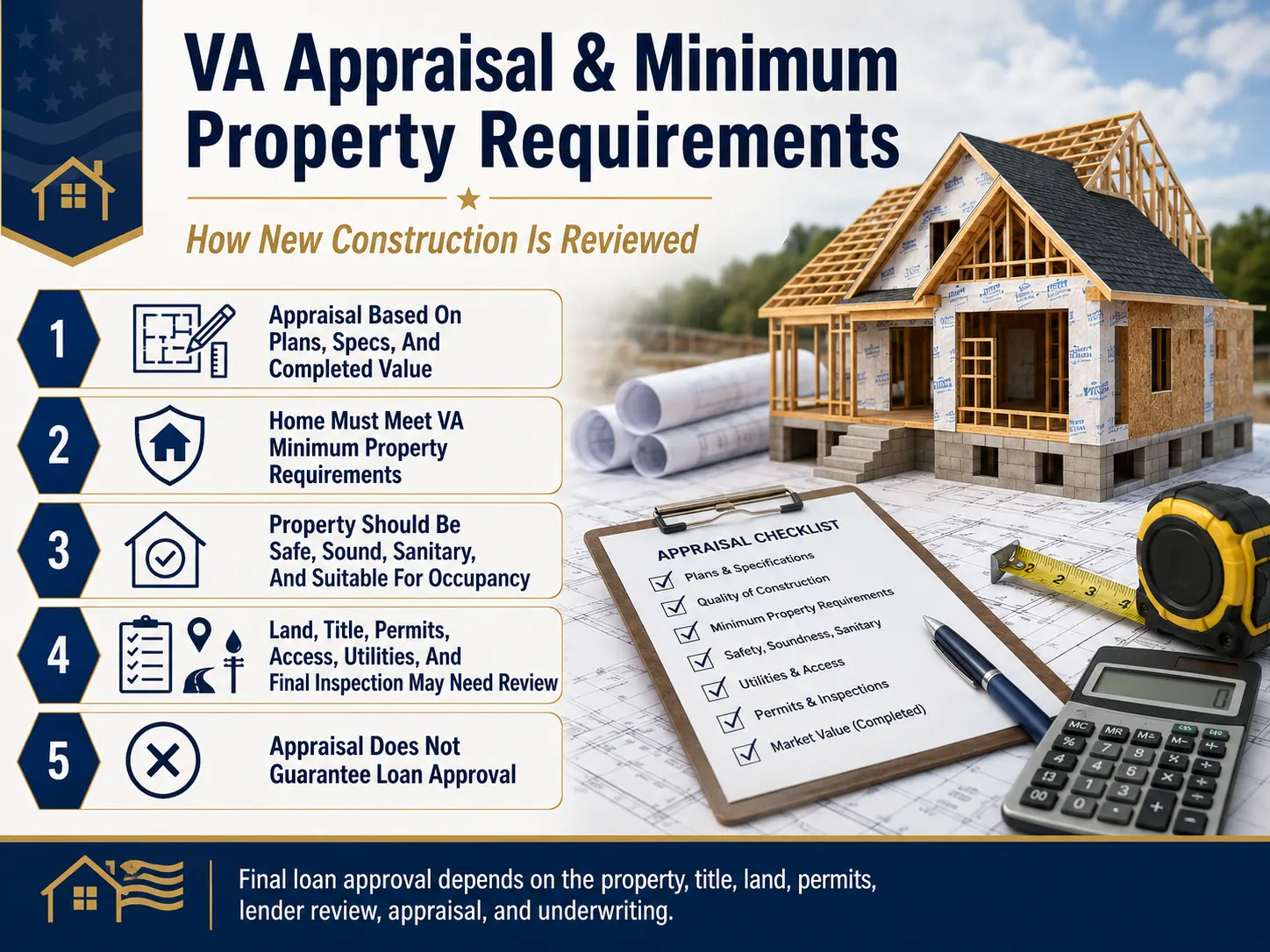

How Do VA Appraisal and Minimum Property Requirements Affect New Construction?

VA construction loans typically require a VA appraisal or property review based on plans, specifications, and completed value. The property must also meet applicable VA minimum property requirements.

A VA appraisal does not guarantee loan approval. The property, title, land, permits, plans, access, utilities, and final inspection may still need review before the loan can move forward.

The completed home generally must be safe, sound, sanitary, and suitable for occupancy. Borrowers can review the official VA Lender’s Handbook, but file-specific guidance should come from the lender and mortgage professional handling the loan.

What Costs Apply to a VA Construction Loan?

A VA Construction Loan does not mean no closing costs. Possible costs may include lender fees, title fees, recording fees, prepaid items, escrow setup, appraisal fees, inspection fees, builder-related costs, and other construction-related costs.

A VA funding fee may apply depending on borrower status, loan use, exemption status, and current VA rules. Some eligible borrowers may be exempt, but exemption must be verified.

Official VA guidance on VA funding fee and closing costs can help borrowers understand what may apply. No down payment may be possible for some eligible borrowers, but this is not guaranteed in every construction scenario.

Borrowers should review a Loan Estimate before making a final decision. The CFPB’s Loan Estimate explainer can help borrowers understand estimated payment, cash to close, loan terms, and closing costs.

If you are comparing land cost, construction budget, closing costs, and long-term affordability, a local review can help you see whether the loan structure fits your goals. This is especially helpful before choosing a builder or making a land decision.

Check VA Construction Loan Options

What Documents May Be Needed for a VA Construction Loan?

VA construction loan documentation may be more detailed than a standard VA purchase loan. The loan file must support both the borrower’s ability to repay and the construction project itself.

Documents may include the Certificate of Eligibility, identification, income documents, employment information, bank statements, credit authorization, builder contract, construction budget, plans and specifications, land documents, insurance information, title information, and permit-related documents if required.

Borrowers can review VA guidance on how to request a Certificate of Eligibility before applying. Lender overlays may affect documentation, especially for construction-to-permanent loans that require extra builder and property review.

How Does a VA Construction Loan Compare With Other Mortgage Options?

A VA Construction Loan may fit eligible borrowers who want to build a primary residence using VA home loan benefits. A standard VA purchase loan may be simpler if the borrower finds an existing home or a newly built completed home.

Borrowers can compare VA loan options with broader mortgage loan options. Some borrowers may also compare conventional loan options, FHA loan options, USDA loan options, or future mortgage refinance options.

VA also provides official VA purchase loan information, which may help borrowers compare building a home with buying an existing property.

Borrowers should compare payment, closing costs, funding fee, construction timeline, builder requirements, appraisal requirements, land costs, equity, one-time close availability, two-time close structure, and long-term goals. No loan option is automatically better for every borrower.

What Mistakes Should Borrowers Avoid With a VA Construction Loan?

VA construction financing can be helpful, but borrowers should avoid assuming it works the same way as a standard VA purchase loan. Construction adds builder, timeline, land, appraisal, and project review layers.

Assuming every lender offers VA construction loans

Assuming VA eligibility means automatic approval

Assuming every builder qualifies

Assuming no down payment applies to every situation

Ignoring VA funding fee and closing costs

Ignoring construction delays

Ignoring change orders and cost overruns

Comparing only the interest rate

Not reviewing the Loan Estimate

Not confirming land or lot requirements

Not asking about one-time close versus two-time close

Not confirming VA appraisal and minimum property requirements

Choosing a builder before understanding lender requirements

Signing a builder contract before checking VA construction loan eligibility

Borrowers should use a VA Construction Loan as a way to compare building options, not as an automatic approval or savings guarantee. The strongest approach is to review VA eligibility, builder fit, land details, costs, and Loan Estimate terms before signing major construction documents.

What Real-Life VA Construction Loan Scenarios Can Tulsa Borrowers Learn From?

Could a Broken Arrow Veteran Build With a One-Time Close VA Construction Loan?

A Broken Arrow Veteran may want to build a primary residence and ask whether one-time close construction financing is available. In this hypothetical case, the borrower should review COE status, entitlement, builder acceptance, land details, appraisal requirements, and Loan Estimate terms before assuming the structure works.

This example does not guarantee approval, no down payment, builder acceptance, appraisal approval, or final loan terms. The outcome depends on VA rules, lender requirements, builder review, property details, and underwriting.

Could an Owasso Borrower Include Land in a VA Construction Loan?

An Owasso borrower may own land or want to include a lot in the overall build plan. The lender would need to review land ownership, title, access, value, appraisal details, construction budget, and loan structure.

This example is educational only. Land and construction structure can vary, so borrowers should confirm details before making an offer on a lot.

Could a Claremore Buyer Compare VA Construction With Buying an Existing Home?

A Claremore buyer may compare building a home with buying an existing property using a standard VA purchase loan. The comparison may involve timeline, builder requirements, closing costs, appraisal review, construction risk, and long-term goals.

Neither option is automatically better. The right choice depends on the borrower’s eligibility, budget, timeline, builder options, property goals, and lender review.

How Should Borrowers Prepare Before Applying for a VA Construction Loan?

Preparation can help borrowers avoid delays before choosing land or a builder. VA construction financing should be reviewed early because the builder, property, loan structure, and borrower profile all matter.

Helpful preparation steps include reviewing:

VA eligibility and Certificate of Eligibility

Entitlement and current budget

Monthly payment comfort level

Construction goal and property location

Land or lot status

Builder options and builder contract

Plans and specifications

Construction timeline and draw schedule

One-time close availability

Two-time close comparison

Appraisal expectations and minimum property requirements

Closing costs and VA funding fee

Loan Estimate and long-term affordability

Credit review, income documents, residual income, and DTI

Borrowers can start with mortgage pre approval guidance to understand what a lender may review before a serious build plan moves forward. Borrowers can also check credit reports through AnnualCreditReport.com before applying.

A VA construction loan review can help you understand eligibility, builder requirements, land questions, Loan Estimate details, and possible loan structure. Reviewing these items before choosing a builder can help reduce costly surprises.

Check VA Construction Loan Options

What Questions Do Borrowers Ask About VA Construction Loans?

What Is a VA Construction Loan?

A VA Construction Loan is a VA-backed mortgage option that may help eligible borrowers build a primary residence. It includes extra builder, appraisal, property, land, and lender requirements compared with many standard home purchase loans.

Who Qualifies for a VA Construction Loan?

Borrowers generally need to be eligible for VA home loan benefits and must meet lender, credit, income, residual income, entitlement, builder, property, and underwriting requirements. Eligibility is not automatic.

Can I Use a VA Loan to Build a Home?

Eligible borrowers may be able to use VA benefits to build a primary residence, but not every lender offers VA construction financing. The builder, property, plans, appraisal, title, and loan structure must be reviewed.

Does a VA Construction Loan Require a Down Payment?

Some eligible borrowers may qualify for VA financing with no down payment, but this is not guaranteed in every construction scenario. Entitlement, loan amount, land, appraisal, lender requirements, and borrower profile can affect the outcome.

Does a VA Construction Loan Require a VA-Registered Builder or Builder ID?

The builder may need to be VA-registered, have a VA builder ID, or meet lender-accepted builder requirements. Borrowers should confirm builder eligibility before signing a construction contract.

Can a VA Construction Loan Include Land?

Land may be reviewed as part of the construction financing structure in some cases, but the details depend on lender rules, title, appraisal, ownership, loan amount, and project structure. Borrowers should confirm land requirements early.

What Is the Difference Between One-Time Close and Two-Time Close Construction Financing?

A one-time close may combine construction and permanent financing into one closing when available. A two-time close may use separate construction financing and permanent mortgage financing. Availability depends on the lender and loan structure.

Should I Compare a VA Construction Loan With Other Mortgage Options?

Yes. Borrowers should compare VA construction financing with a standard VA purchase loan, conventional construction loan, FHA, USDA, and other options based on costs, timeline, builder requirements, appraisal, and long-term goals.

What Should Borrowers Know Before Relying on This VA Construction Loan Guide?

VA Construction Loan information is educational only and should be reviewed for accuracy by a licensed mortgage professional before publishing or relying on it for a loan decision.

VA construction financing does not guarantee approval, no down payment, builder acceptance, appraisal approval, construction completion, lower costs, lower rate, or final loan terms. Loan approval depends on VA eligibility, Certificate of Eligibility, entitlement, credit, income, residual income, debt-to-income ratio, loan program rules, lender requirements, builder review, property review, appraisal, title review, and underwriting.

Information may change, so borrowers should confirm current VA guidelines, funding fee rules, builder requirements, appraisal requirements, closing costs, and program requirements. The CFPB’s Closing Disclosure explainer can help borrowers review final loan details before closing.

Last Updated: 3rd June 2026

Reviewed By: Alfredo Madrid , NMLS #266006